Cold Chain Market Share, Demands, Supply and Forecasts 2028

Cold Chain Industry Overview

The global cold chain market size is estimated to reach USD 628.26 billion by 2028, according to a new study by Grand View Research, Inc., registering a CAGR of 14.8% from 2021 to 2028. Technological advancements in the packaging, processing, and storage of seafood products are expected to drive the market over the forecast period. Cold chain solutions have become an integral part of Supply Chain Management (SCM) for the transportation and storage of temperature-sensitive products. Increasing trade of perishable products is anticipated to drive product demand over the forecast period.

Cold Chain Market Segmentation

Grand View Research has segmented the global cold chain market on the basis of type, packaging, equipment, application, and region:

Based on the Type Insights, the market is segmented into Storage, Monitoring Components and Transportation.

- In terms of revenue, the storage segment accounted for the largest revenue share of more than 58% in 2020 and will retain the dominance over the forecast period owing to increasing preference for packaged foods across the globe. Changing dietary patterns and lifestyles of consumers is driving the demand for frozen foods. This is expected to boost the demand for storage solutions.

- The use of monitoring components in the cold chain is particularly increasing. This growth can be attributed to the technological advancements and growing need to ensure the integrity, efficiency, and safety of shipments. Advances are equally noticeable in backend IT infrastructure and frontend devices deployed for collecting and reporting real-time shipment information.

- Cold chain systems are crucial for supplying food, beverages, and healthcare products. Demand for high-cube refrigerated trailers, connected refrigerated trucks, insulated containers, and vehicles favoring cross-product transportation is expected to drive the transportation segment over the forecast period.

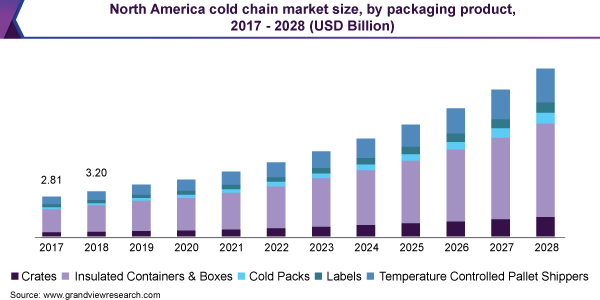

Based on the Packaging Insights, the market is segmented into Product, and Materials.

- The product packaging segment held the largest revenue share of over 73% in 2020. The product segment includes a detailed analysis of crates, insulated containers and boxes, cold packs, labels, and temperature-controlled pallet shippers.

- The materials segment includes an in-depth analysis of insulating materials and refrigerants. The insulating materials and refrigerants are considered complete systems for temperature-sensitive products. The insulating materials segment is further classified into Expanded Polystyrene (EPS), Vacuum Insulated Panel (VIP), Polyurethane (PUR), cryogenic tanks, and others.

Based on the Equipment Insights, the market is segmented into Storage Equipment and Transportation Equipment.

- The storage equipment segment accounted for the largest revenue share of over 75% of the global market in 2020. Storage equipment is crucial in the refrigerated storage industry as they ensure the quality of products and increase their shelf life. The equipment used includes refrigerators, deep freezers, vaccine carriers, and others. Storage equipment is further divided into on-grid and off-grid.

Based on the Application Insights, the market is segmented into Fruits & Vegetables, Fruit Pulp & Concentrates, Dairy Products, Fish, Meat, and Seafood, Processed Food, Pharmaceuticals, Bakery & Confectionary, and Others (Ready-to-Cook, Poultry).

- The fish, meat, and seafood segment led the global market accounting for the highest revenue share of 24% in 2020, and will retain the leading position growing at a steady CAGR from 2021 to 2028. Technological developments in the processing, packaging, and storage of seafood are anticipated to stimulate the growth of this segment.

- High product demand in the pharmaceuticals segment can be attributed to its importance in maintaining the efficacy and safety of pharmaceuticals. The cold chain in the pharmaceutical industry is driven by stringent regulatory norms, such as Goods Distribution Practices (GDP) in the European Union (EU).

Cold Chain Regional Outlook

- North America

- Europe

- Asia Pacific

- South America

- Middle East

- Africa

Key Companies Profile & Market Share Insights

Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. Vendors have adopted Hazard Analysis and Critical Control Points (HACCP) and RFID technologies to improve efficiency with a decreased size of shipments.

Some prominent players in the global cold chain market include

- Agro Merchant Group (U.S.)

- Nordic Logistics and Warehousing, LLC (U.S.)

- Preferred Freezer Services, LLC (U.S.)

- Cold Chain Technologies, Inc. (U.S.)

- Cryopack Industries, Inc. (U.S.)

- Creopack (Canada)

- Cold Box Express, Inc. (U.S.)

Order a free sample PDF of the Cold Chain Market Intelligence Study, published by Grand View Research.